Manscaped SPAC

A $1 billion valuation for grooming down there?!

1/ I should dive into serious health care S-1s (and will). But it’s hard to resist that @manscaped SPAC. It’s a super-charged version of Dollar Shave Club with great tongue-in-cheek branding, but has its marketing efficacy hit a wall?

2/ I don’t know if you could call it soulful, but @manscaped certainly knows its young male audience. Look at these products: the weed whacker, the lawn mower, the crop preserver. The brand is brilliant.

3/ Like every other Instagram brand, there is the inevitable social cause (and, of course, the amount of the donation is not quantified).

4/ So, what’s impressive here? From a cold start in 2018, the brand now claims to have 41% aided brand awareness. You can’t listen to a Joe Rogan, Dave Portnoy or Bill Simmons podcast without hearing those commercials. They are all over NASCAR, stadiums, TV, etc.

5/ @manscaped has seen explosive revenue growth. The below chart shows trailing twelve month revenue by quarter. It’s grown off of less than $20M in venture funding and has had positive adjusted EBITDA (taking out equity compensation) for the past couple years.

6/ Like almost every e-commerce company I can think of, @manscaped is having post-COVID D2C growth challenges. After flying out of the gate, U.S. D2C will grow only 9.4% this year. You can see the broader growth challenge by looking at QoQ revenue growth.

7/ We’ll get back to growth later, but lets first look at subscription economics. 70% of 1st time buyers are on subscription (getting replacement blades for $15 every 3 months), but we see no retention data or LTV:CAC data in the @manscaped deck. Are they hiding something?

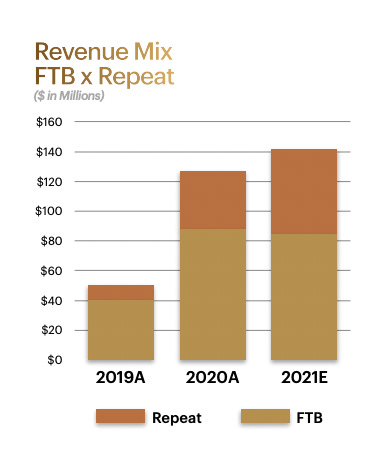

8/ On a positive note, @manscaped is incrementally growing 1st time buyer AOV, from $60 in 2019 to $90 today. Repeat as a percent of sales is now 40%, up from 20% two years ago. I wonder how much of the repeat is blades versus other consumables like shaving gel, ball toner(?!), et al.

9/ Let’s try to suss out unit economics. They spent $100.8M to acquire 1.1M new patients in 2020, for a ~$92 CAC , up from ~$68 in 2019 (+35.3% YoY). Let’s use a 50% gross margin at a $90 AOV - they are generating $45 in contribution on a first order.

10/ If you look at the repeat revenue, it is less in aggregate in 2021 than 1st time buyer revenue in 2020. So that year 2 revenue for customers is well below year 1 and payback on D2C is inevitably longer than 2 years.

11/ But… just because paid marketing isn’t effective when applied only to D2C does not mean the overall business is challenged. That paid spend drives revenue across all @manscaped channels and the business is generating EBITDA. Marketing attribution here is enormously challenging.

12/ @manscaped has four strong avenues for growth: (1) Channel expansion; (2) International; (3) Product expansion and (4) M&A. By meeting customers where they are, @manscaped can fulfill the demand created with their high brand awareness.

13/ Let’s start with channel expansion: new channels are still small but highly promising. Marketplace (Amazon) grew 53% YoY and US retail is up 79% YoY. I wish we had more data on US retail - they are in 3,500 doors now but what’s the growth plan? How has sell-through trended?

14/ On the international front, @manscaped >100% growth to >$60M this year was impressive. Future plans are ambitious. I wish we had more data on how much of this is from wholesale v Amazon v D2C. And god forbid they show us unit economics for the international business.

15/ On product expansion, the question is do they have license to own his bathroom. They are launching shampoo and body wash, along with deodorant and cologne this year. I’m bullish here: past is often prologue and customers have increased spending/AOV with @manscaped over time.

16/ What can go right for @manscaped: (1) leverage their brand awareness to drive a highly profitable wholesale businesses, with D2C becoming less important; (2) they own the bathroom, taking over more shelf space at stores and in mens’ bathrooms; (3) the brand is global and ubiquitous.

17/ The SPAC pegged @manscaped value at $1B - seems high. We lack so much data on unit economics, store sell through, etc. and much of the growth story is on the come. Give them credit for a mature EBITDA margin of 15% and trading at 15-20x —> 2.25-3x 2021 revenue? $650-$890M?

Dollar Shave Club v2.0 in the age of Covid YouTube audience from 2020... excellent product/brand positioning; they can post beyond Axe and ultimately get acquired by same company - Unilever. (DHC, Axe, Manscaped)... house of male -brands...