Boxed and Grove SPACs

More venture bets going public well before they're predictable (or, um, ready)

1/ S-1 Teardown: Boxed and Grove. Online grocery has gone through a proverbial whipsaw, with a huge COVID bump and subsequent pullback. Let’s look at this through @BoxedWholesale, which started trading today, and Grove Collaborative (@ePantry), which announced its SPAC merger yesterday.

2/ Boxed sells bulk, high-repeat essentials, serving B2B and B2C customers with a membership model analogous to @Costco. Its SPAC presentation emphasizes how they also sell advertising and have launched a 3rd-party seller marketplace https://www.sec.gov/Archives/edgar/data/1828672/000110465921099170/tm2123936d1_425.htm

3/ Grove is focused on being a leading purveyor of natural health and personal care products. Leads with an ESG story around sustainability and “doing well by doing good.” https://static1.squarespace.com/static/614ca8a736f23f32d28470c2/t/61b10601d545a75202a71671/1638991379188/Grove+Collaborative+Presentation+12.8.21.pdf

4/ @BoxedWholesale is also telling an ESG story - less waste, majority minority employees, fighting inequality, et al. This just seems like table-stakes for domestic D2C companies these days. Question: how much of a valuation premium will an ESG story provide over time?

5/ @BoxedWhole and Grove have very different customer bases. 42% of Boxed customers are rural, single renters who live far from Costco. Only 11% are urban and close to Costco. For Grove, their customers are very much what you expect - college educated in major metros.

6/ So how big can these get? Let’s look at the grocery e-commerce market. It was $106B in 2020 (10% of total). The Boxed investment deck claims this will grow to $248B in 2025 but that doesn’t match the facts on the ground. The U.S. online grocery market posted $7 billion in sales in May, down 16% YoY. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/retailers-continue-online-grocery-investments-despite-slowing-sales-65122812

7/ This begs the question of how much customers actually want grocery delivery vs. the store experience.

8/ @BoxedWholesale saw a woeful drawback in 2021 after a nice COVID bump. It increased advertising 600% in order to grow 14% YoY. Put another way, it spent $30M in additional advertising to grow revenue by $25M and gross margin by $5M. Not good.

9/ Boxed also gives no data on customer retention, cohort data or LTV:CAC in its deck. Only reason to not show that is the data are not strong.

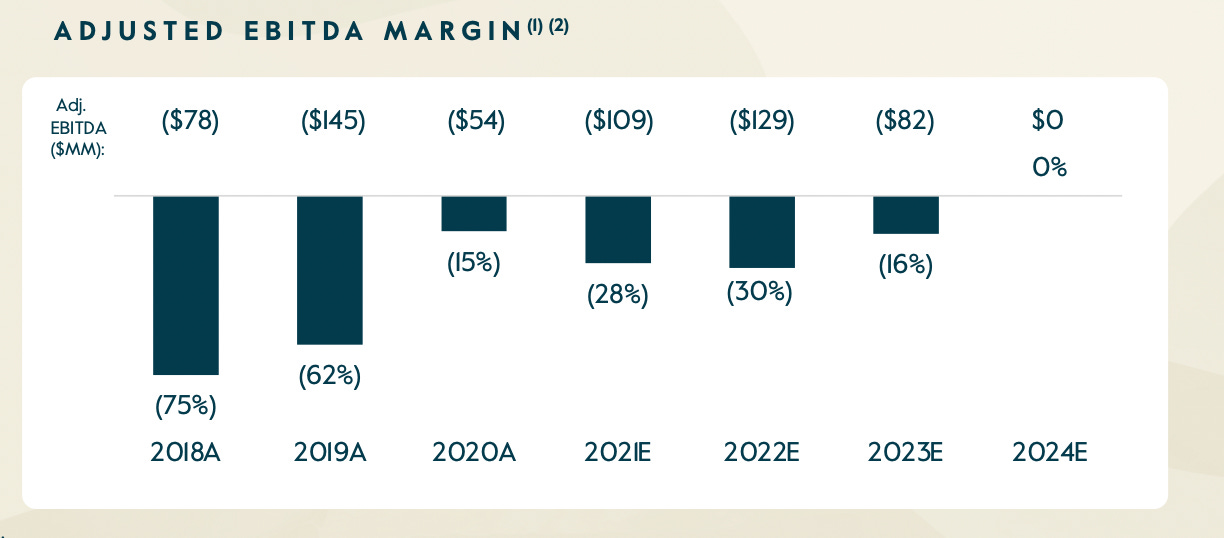

10/ Grove has a story that rhymes with Boxed, with more potential imho. They too saw a massive bump in COVID, growing 56% in 2020, which slowed to only 6% YoY in ’21. Buying even that small amount of growth in ’21 was incredibly expensive. Grove will show ($109M) in adjusted EBITDA this year off of only $364M in revenue.

11/ That said, Grove has a brand customers love, as shown by really strong net revenue retention of ~50% even 5 years after signup. The flip side to that is customer acquisition is very expensive and, as a result, they target 2-3x LTV/CAC over 5 years. Best in class is 3:1 in 24 months or less.

12/ Growing online is just very hard these days - with high customer acquisition costs and a finite pool of customers. It only works with high recurrence and high contribution margin per order, a combination that neither Grove nor Boxed has.

13/ So why do I like Grove more than Boxed? Both are highly speculative but I question the fundamentals of Boxed’s base business - as I see no evidence customers are loyal and rabid. Grove has brand love, proprietary products and A LOT more levers to pull.

14/ Grove is focused on its own proprietary CPG products, launching 160 new SKUs per year in categories ranging from soap to detergent to deodorant and shampoo. Can Grove build a green @Clorox or @Unilever?

15/ Grove has a big omni-channel opportunity and successfully launched in @Target in April and then launched @Amazon in Dec. They have 3 new retail partnerships confirmed for 2022 and lots more in the pipe. International provides additional upside. And the brand awareness lift from retail distribution will certainly help the e-commerce business.

16/ All that said, Grove doesn’t even break out wholesale sales in its SPAC presentation, meaning these are still very small. Their online business requires a lot of scale to get to the promised land and growth is hard. Optimally, Grove would undergo this omni-channel transformation as a private company. I guess the SPAC is the cheapest way for them to raise capital right now.

17/ Now let’s turn to Boxed. Their only option to drive value creation is to optimize its online business. One area is broadening assortment to generate higher revenue per order. Boxed has 2K SKUs today compared to 4-7K at Costco. Potential expansion categories are pet, baby, beauty, home goods, fresh food and vitamins.

18/ The next place for Boxed to add value is via higher frequency and loyalty. Boxed just launched Autosave, its version of Amazon Subscribe & Save. They also have an annual membership program, with 36K users paying $49 a year, accounting for 17% of revenue.

19/ Yet another path for Boxed is increased margin. Lots of ways to do it: (1) Private label: is 14% of sales, with 6% higher net product margin than 3rd-party product; (2) higher AOV —> lowers shipping cost; (3) higher capacity utilization / expanded margin with scale. Boxed aims to grow margin from 14% to 24% by 2026.

20/ A third way for Boxed to increase value is via other related lines of business: (1) advertising; (2) B2B sales (only 10% today for Boxed); (3) opening up 3rd-party marketplace, where vendor partners sell on their platform and do their own logistics.

21/ A final way for Boxed to create value is via the equivalent of AWS - selling its proprietary omni-channel e-commerce software to others. Is that a real opportunity? They expect to do $12M in 2021 and $13M in 2022 with Aeon as their only customer. Of course, they predict hockey stick growth after that. Hard to place a value on this!

22/ Sounds like Grove has to make wholesale work meaningfully to build a valuable business. Boxed is throwing a lot of stuff against the wall and praying something sticks.

23/ The SPAC Seven Oaks is valuing Boxed at $647M or 2.8x forecasted 2021 revenue. Very rich for a low growth e-commerce business with uncertain near-term prospects. Grove is being valued at $1.5B pre-money or 3.9x 2021 revenue.

24/ Of course, these brands could be compared to @Chewy, which has 22.4% gross margin, 26.8% YoY growth, spitting out cash and valued at 3.2x TTM revenue. We could also use @HelloFresh, which is trading at 2.5x TTM revenue, generating real EBITA and growing 46% YoY.

25/ Despite some challenges, Chewy and Hello Fresh show you can build really great long-term compounding businesses in grocery and related areas, with good unit economics at scale. Unfortunately, neither Grove or Boxed show the same promise as these two market giants - they have worse economics, lower growth and uncertain prospects.

26/ While it feels that Grove could build a big green CPG business, there’s a lot of wood to chop. Boxed just feels highly speculative. These companies feel in many ways like early stage venture-backed businesses, not predictable businesses ready for the public markets. Time will tell if the markets see it differently.

Another great precis from Jason; enjoyed this: "While it feels that Grove could build a big green CPG business, there’s a lot of wood to chop"