Aussie fast fashion giant storms the U.S.

AKA Brands and Princess Polly come out of nowhere to be a major fast fashion player

1/ TLDR: a.k.a. Brands, the best apparel IPO since Canada Goose & Moncler, priced this week at $2.2B. Parent of @princesspolly @culturekings has used TikTok, creative loyalty programs and SMS marketing to fuel explosive growth. Along with @shein shows continued share shift for Gen Z from @zara @hm to new digitally driven fast fashion brands

2/ Kind of a nexgen @vfcorp or a less sketchy @boohoo, A.K.A. Brands is a brilliantly executed roll up from Summit Partners. Historically driven by Aussie fast fashion brand @princesspolly, AKA recently acquired Aussie streetwear giant @culturekings as well. For the purpose of this thread I want to focus on the explosive emergence of @princesspolly into US fashion

3/ @princesspolly launches well over a decade ago in Australia, building the infrastructure to add 500-800 new styles a week. Then in April 2019 it launches in the US with a super smart social strategy focusing on influencers on YouTube and TikTok producing a seemingly unlimited number of haul videos.

4/ @princesspolly scales from $45m in 2019 to $125M in 2020 in the US alone and continues to accelerate. Now ranks #5 of all fashion brands for teens. https://www.forbes.com/sites/markfaithfull/2021/04/19/how-princess-polly-stormed-the-us-teen-market-with-tiktok-try-on-hauls/?sh=190d97ccb3e0

5/ Note how the 1st generation of DNVBs used Instagram and FB, along with traditional media, to build brand awareness. That’s shifted to influencer marketing on YouTube and TikTok. If our @maveron portfolio is any indication, A.K.A. has built the systems to determine how to gift free product to their 13K influencers, measure cost per impression and derive a return on investment for each one of them

6/ Several brand differentiators from @shein @fashionnova. First and foremost, those brands have notoriously sketchy labor practices and aka looks squeaky clean in comparison. Second, they claim a sustainability focus, a bit of an oxymoron for a fast fashion business. That said, they promise to have over 20%+ of products made with lower-impact materials by 2022, 60% by 2025, and 100% by 2030.

7/ 190 million site visits, with 70% from mobile. Foreshadows how every generation will shop primarily on their phones in the not so distant future. Also I’d love to see what percent of new customers come via each channel, but it’s not broken out here at all besides saying 62% of traffic is from organic sources, which tells us nothing.

8/ A few things worth noting. their S-1 claims an impressive full price sell through of 80%. There is no way that is the case today. Look at the discounting on their homepage!

9/ Surprised they derive only 54% of revenue from owned brands. I imagine this goes up over time as it’s just so hard to make money on 3rd party brands. They certainly drive a lot of traffic to their site with brands like Doc Martens and Levis, but at the expense of margin

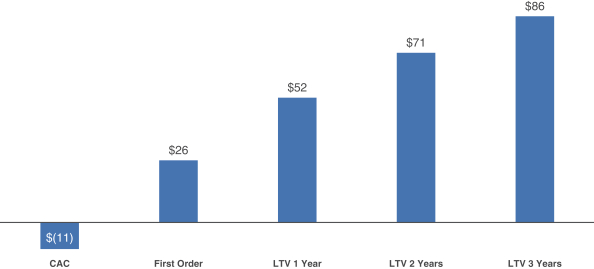

10/ Says it has a one year LTV/CAC of 3.1 for the 2019 Australian customer cohort. This doesn’t tell us anything at all. It’s a different world - what does America look like and CACS are orders of magnitude higher now - please give us something more here!

11/ If the below holds true, they generate $52 in contribution in year one and then $19 and $15 in the subsequent two years. I would’ve expected revenue retention to be higher, frankly. With online CACs > $40 for many brands, how long can they keep acquiring new customers cheaply enough to sustain a strong LTV/CAC

12/ Curious if they can move the dial on their loyalty program, which gives access to events, priority for drops and special Facebook group to top spenders. I often struggle with ROI of loyalty programs but these more psychological benefits of being “in the club” are interesting and powerful

https://us.princesspolly.com/pages/rewards

13/ Despite my grumbling above, Marketing is impressively < 10% of sales. This compares to 19% for Warby. And the business is profitable - not profitable with some strange non-GAAP adjusted EBITDA metric but actually profitable. Generated over $20M in free cash flow in 2020

14/ The bull case here: online apparel is an enormous category, where online penetration is going to 50% from 37.5% today. Princess Polly has a marketing engine fueled by social media and has a pulse on culture that sustains. The parent company, AKA, can keep acquiring new businesses and use its infrastructure as rocket fuel

15/ The bear case here. Brands come in and out of favor faster than ever before. Will something that has catapulted to popularity this fast have what it takes to endure - is there true emotional connection with this brand for customers that can last a decade. Or will the next buzzy fast fashion brand overtake it

16/ One last brief aside. In reading, the S-1 I was struck by the complexity of these PE org structures. I’m used to a world where companies create value through growing sales vs using complex financial engineering. This structure probably generated enough legal fees to create generational wealth for an army of lawyers